Local Government: Results of the 2010–11 Audits: Message

Ordered to be printed

VICTORIAN GOVERNMENT PRINTER November 2011

PP No 86, Session 2010–11

Ordered to be printed

VICTORIAN GOVERNMENT PRINTER November 2011

PP No 86, Session 2010–11

In accordance with section 16A and 16(3) of the Audit Act 1994 a copy of this report, or relevant extracts from the report, was provided to the Department of Treasury and Finance, the Department of Sustainability and Environment, the Valuer-General Victoria, the Essential Services Commission, the State Owned Enterprise for Irrigation Modernisation in Northern Victoria and the 20 entities with a request for submissions or comments.

Responses were received as follows:

This Appendix sets out the performance indicators against which water entities are required to report. Financial Reporting Direction 27B Presentation and Reporting of Performance Information specifies the entities required to prepare and submit for audit a performance report. Ministerial directives issued under section 51 of the Financial Management Act 1994 specify the performance indicators that need to be reported in a performance report.

Indicator |

|---|

This Appendix details the overall financial sustainability assessment of each entity over the past five years given six indicators.

The overall financial sustainability risk assessment has been calculated using the ratings determined for each indicator as outlined in Figure F1. Appendix E provides further information on each indicator.

Figure F1

Overall financial sustainability risk assessment

This Appendix sets out the financial indicators used in this report. The indicators should be considered collectively, and are more useful when assessed over time as part of a trend analysis. The indicators have been applied to the published financial information of the 19 water entities for the five-year period 2006–07 to 2010–11.

This Appendix presents the composition of revenue, expenses, assets and liabilities at an industry, metropolitan, regional urban and rural level.

Figure D1

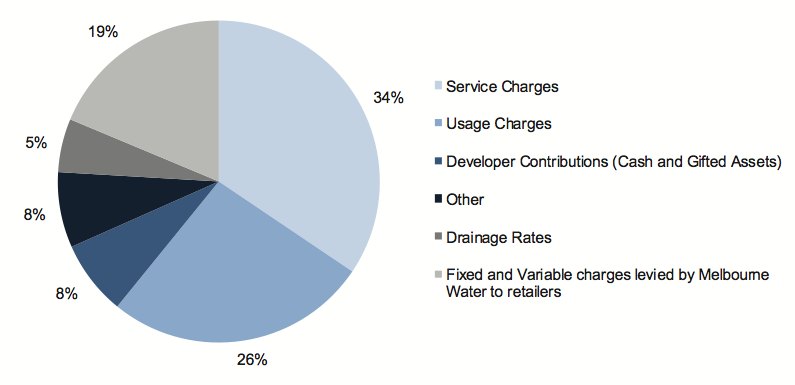

Revenue composition

Source: Victorian Auditor-General's Office.

Figure D2

Expense composition

Audit types |

Financial report | |||

|---|---|---|---|---|

The responsible minister for the water industry is the Minister for Water. The relationship between the Minister for Water and the water entities is established by the Water Act 1989 and the Water Industry Act 1994.

The Water Group, a business unit within the Department of Sustainability and Environment, supports and advises the Minister for Water.

The 19 entities also report to the Treasurer of Victoria.

| AAS | Australian Accounting Standard |

| AASB | Australian Accounting Standards Board |

| CRC | Current Replacement Cost |

| DRC | Depreciated Replacement Cost |

| DSE | Department of Sustainability and Environment |

| DTF | Department of Treasury and Finance |

| ESC | Essential Services Commission |

| FMA | Financial Management Act 1994 |

| FRD | Financial Re |