Water Entities: Results of the 2011–12 Audits: Message

Ordered to be printed

VICTORIAN GOVERNMENT PRINTER November 2012

PP No 194, Session 2010–12

Ordered to be printed

VICTORIAN GOVERNMENT PRINTER November 2012

PP No 194, Session 2010–12

In accordance with section 16(3) of the Audit Act 1994 a copy of this report, or relevant extracts from the report, was provided to the Department of Health and named hospitals with a request for submissions or comments.

The submission and comments provided are not subject to audit nor the evidentiary standards required to reach an audit conclusion. Responsibility for the accuracy, fairness and balance of those comments rests solely with the agency head.

Responsibility of public sector entities to achieve their objectives, with regard to reliability of financial reporting, effectiveness and efficiency of operations, compliance with applicable laws, and reporting to interested parties.

Establishing control of an asset, undertaking the risks, and receiving the rights to future benefits, as would be conferred with ownership, in exchange for the cost of acquisition.

This Appendix sets out the financial indicators used in this report. The indicators should be considered collectively and are more useful when assessed over time, as part of a trend analysis. The indicators have been applied to the published financial information of the 87 public hospitals for the five year period 2007–08 to 2011–12.

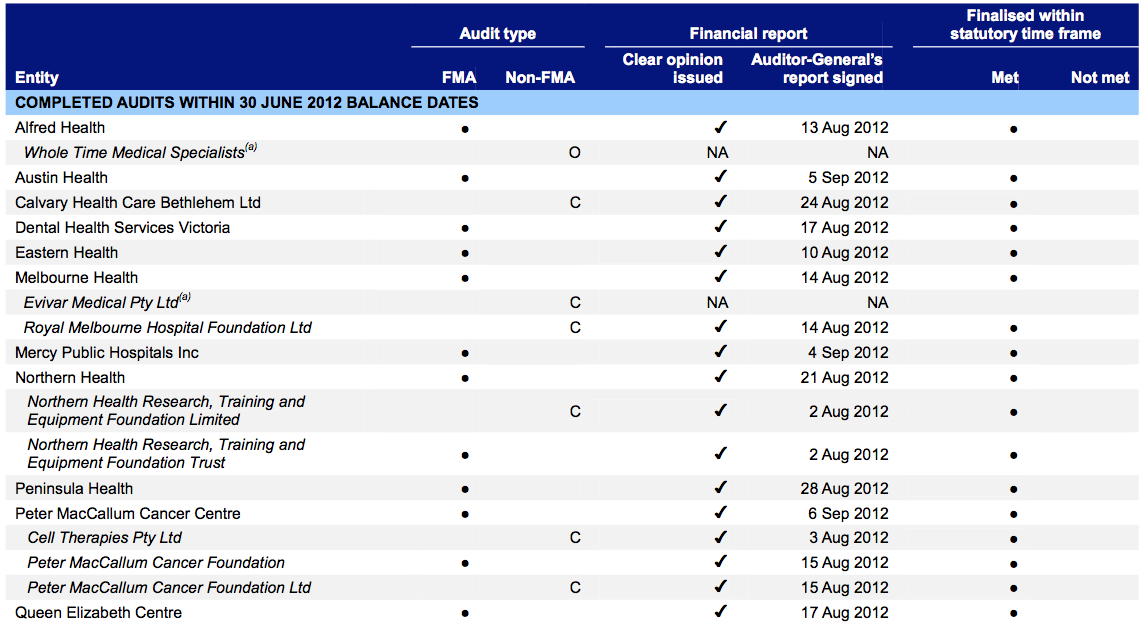

(a) At the date of this report, the financial audit of this entity was not complete and was not included as part of the statutory time frame metric.

This report is second of six reports to be presented to Parliament covering the results of our audits of public sector financial reports. The reports are outlined in Figure A1.

Figure A1

VAGO reports on the results of the 2011–12 financial audits

Report |

Description |

|---|---|

Auditor-General’s Report on the Annual Financial Report of the State of Victoria, 2011–12 |

Effective internal controls enable entities to meet their financial and governance objectives and deliver reliable, accurate and timely financial reports. This Part presents the results of our assessment of general internal controls and controls over audit committees, capital projects and self-generated revenue.

To be financially sustainable, entities need to be able to meet current and future expenditure as it falls due. They also need the ability to absorb foreseeable changes and materialising risks without significantly changing their revenue and expenditure policies. This Part provides our insight into the financial sustainability of public hospitals based on our analysis of the trends in key financial indicators over a five-year period.

Accrual-based financial statements enable an assessment of whether public hospitals are generating sufficient surpluses from operations to maintain services, fund asset maintenance and retire debt.

This Part analyses the financial results of Victoria’s public hospitals and their associated entities for the year-ended 30 June 2012.

The combined financial results for public hospitals in 2011–12 included: