Organisational Sustainability of Small Councils

Overview

Over the past five years, the reliance of audited councils on government grants has grown substantially. While rates and charges have increased in real terms, this has not been enough to keep pace with councils' increases in costs. Several audited councils are projected to have deteriorating positions against key financial indicators, which places them at a higher risk of short-term and immediate sustainability concerns.

Common sustainability issues and challenges across the audited councils include having effective financial planning and asset management, effectively and efficiently delivering services, recruiting and retaining qualified and skilled staff and dealing with the impact of population change. A range of strategies and actions have been implemented to address these issues and challenges, however, councils generally cannot demonstrate their effectiveness and whether they are having a material impact on improving their sustainability. Further work is required to improve long-term financial planning, asset management and service delivery, and to address specific challenges.

Local Government Victoria (LGV) provides a range of general guidance and support to councils, and it has implemented actions to assist small councils at high-risk of sustainability issues. However, it could more proactively target small councils with appropriate support and advice before their situation becomes critical. LGV is developing a performance reporting framework to provide a common suite of sustainability indicators for councils. This may provide an opportunity for LGV to more closely monitor councils' sustainability and respond appropriately to support them on a timely basis.

Organisational Sustainability of Small Councils: Message

Ordered to be printed

VICTORIAN GOVERNMENT PRINTER June 2013

PP No 233, Session 2010–13

President

Legislative Council

Parliament House

Melbourne

Speaker

Legislative Assembly

Parliament House

Melbourne

Dear Presiding Officers

Under the provisions of section 16AB of the Audit Act 1994, I transmit my report on the audit Organisational Sustainability of Small Councils.

Yours faithfully

Dr Peter Frost

Acting Auditor-General

12 June 2013

Audit Summary

There are 79 local governments in Victoria. Of these, 21 are classified as small councils with populations of less than 20 000 people. These councils are located in rural areas and administer 89 893 square kilometres, or 40 per cent of Victoria's total area, and serve 217 000 people—4 per cent of the population.

Small councils are heavily dependent on government grants to continue operating. In 2011–12, small councils generated operating revenue of $701 million, with government grants accounting for $360 million, or 51 per cent, and rates and charges contributing $216 million or 31 per cent. In contrast, government grants account for around 22 per cent and rates around 49 per cent of total revenue across all 79 councils.

Organisational sustainability means that councils have the capacity to function efficiently, effectively and economically to meet the current and future needs of their communities to an acceptable standard. Small councils should have a sound understanding of the issues and challenges impacting their sustainability and develop appropriate strategies to mitigate their impact as much as possible. Council operations should be underpinned by effective financial planning and asset management, and effective and efficient service delivery.

The audit assessed whether councils had:

- a sound understanding of the sustainability challenges and issues

- developed appropriate strategies that consider a range of options for addressing sustainability issues and challenges

- evaluated how effective sustainability strategies have been

- been provided with appropriate guidance and support by Local Government Victoria (LGV).

Conclusions

Over the past five years, the reliance of audited councils on government grants has grown substantially. While rates and charges have increased in real terms, this has not been enough to keep pace with councils' increases in costs. Several audited councils are projected to have deteriorating positions against key financial indicators, which places them at a higher risk of short-term and immediate sustainability concerns.

The audited councils generally have a sound understanding of the sustainability challenges they face and have implemented a range of strategies to address these. However, the councils generally cannot demonstrate the effectiveness of strategies and actions and whether these are having a material impact on improving their sustainability.

While four of the audited councils have recently developed long-term financial plans, and all have made some efforts to improve asset management, further work is required in these areas. Councils' existing asset management plans contain out‑of‑date information, which provides limited assurance that asset management requirements are being appropriately considered. Councils have not undertaken comprehensive service reviews and cannot demonstrate that they are delivering services effectively and efficiently, or that they have exhausted all opportunities to introduce or increase user fees and charges. While improving long-term financial planning, asset management and service delivery may not provide assurance that a council will be sustainable, these actions are still necessary in order to remain viable in the medium to long term.

Common sustainability issues and challenges across the audited councils include:

- having effective financial planning and asset management

- effectively and efficiently delivering services

- recruiting and retaining qualified and skilled staff

- dealing with the impact of population ageing and/or population change—such as high growth or decline

- dealing with the defined benefits superannuation shortfall.

LGV provides a range of general guidance and support, which is applicable to small councils in addressing some sustainability concerns, and it has implemented actions to assist small councils at high-risk of sustainability issues. However, LGV could more proactively target small councils with appropriate support and advice before their situation becomes critical. LGV is developing a performance reporting framework to provide a common suite of sustainability indicators for councils. This may provide an opportunity for LGV to more closely monitor councils' sustainability and respond appropriately to support them on a timely basis.

Findings

Financial trends

Over the past five years, the reliance of audited councils on government grants has more than doubled from $33.766 million in 2007–08 to $72.434 million in 2011–12. This equates to an average increase of 25 per cent per year for the audited councils. The increase in grants as a proportion of total revenue averaged 1.9 per cent a year. Over the same period, rates and charges, and user fees and charges increased from $35.714 million to $49.083 million and $7.275 million to $8.810 million respectively. While rates and charges have increased in real terms, they have decreased as a proportion of total revenue, with councils' reliance on these declining over the same period by 1.4 per cent per annum and 0.3 per cent respectively. Therefore, while councils have increased the amount of own-source revenue they generate through rates and user charges, it has not been enough to keep pace with their increase in costs. Given current Commonwealth and State Budget positions and the economic climate, the audited councils' increasing reliance on grants may be unsustainable.

Buloke and Yarriambiack are projected to have deteriorating positions against key financial indicators related to short-term and immediate sustainability concerns. Strathbogie has some worrying financial indicators, but others are projected to improve. Several longer-term financial sustainability indicators are projected to deteriorate for Golden Plains and one for Towong, although Towong is projected to improve against all other indicators.

Effective financial planning and asset management

Effective long-term financial planning and asset management is crucial to sustainability and these should be appropriately integrated so that asset management needs are adequately considered in financial planning. All audited councils except Yarriambiack have recently developed long-term financial plans, but these vary in quality and are not sufficiently integrated with asset management. While the plans—particularly Strathbogie's—reflect a number of better practice elements, further work is needed by all councils to address deficiencies and effectively plan their finances over the long term to support their sustainability.

Effective and efficient service delivery

Councils deliver a wide range of services to their communities. Even within the context of necessary expenditures, there is scope to decide the services and service levels there should be. The Local Government Act 1989 sets out the Best Value Principles that should inform council decisions on services. Other than narrow reviews of specific services—such as to identify cost savings—none of the audited councils have undertaken comprehensive reviews of services in accordance with these principles, or reviewed service levels to assess the effectiveness and efficiency of service delivery. The current approaches provide limited assurance that expenditure on service delivery is informed by an adequate understanding of community needs or the effectiveness and efficiency of council services. All councils have committed to maintaining existing service levels.

Recruiting and retaining qualified and skilled staff

Small councils in regional and rural areas face challenges in attracting and retaining appropriately qualified and skilled staff. All audited councils except Yarriambiack identified this as an issue and some have implemented strategies to address these challenges.

Golden Plains has developed a workforce plan, which contains a number of better practice elements, including identifying future workforce needs and strategies to address workforce issues. While there have been no formal evaluations of the plan itself, council advised it has been effective in informing decisions about staff levels, identifying gaps, career planning for existing staff and potential replacement of key staff.

Strathbogie completed an organisational review in 2011, which included voluntary redundancies, the creation of several new positions and the development of a new organisation structure. While the review recommended that Strathbogie develop a workforce plan, council has not yet done so.

Councils also outsource some positions, including statutory roles, such as building surveyors and planning officers. While Yarriambiack advised that staff recruitment was not an issue, it too outsources these statutory positions. Councils advised that these roles can be difficult to fill and that this may be due to their remuneration being uncompetitive, potential applicants not wanting to relocate to regional areas or because councils only require part-time positions.

Outsourcing may address the issue in the short term and maintain ongoing service delivery. However, councils have not assessed whether this is more cost effective than employing staff directly, and sustainable in the long term.

Population ageing and/or population changes

Population ageing and/or population changes—such as high growth or decline—can present challenges to small councils. Population changes affect councils' rating base and change service delivery needs. With the exception of Towong, there are consistent trends facing the audited councils across the 30-year period—2001 to 2031—of either increasing (Golden Plains, Strathbogie) or decreasing populations (Buloke, Yarriambiack). All audited councils except Yarriambiack have developed, or are developing, strategies related to population change. However, these are relatively new or in development.

Defined benefits superannuation shortfall

A sharp increase in employee benefit expenses in 2012 for all audited councils is due to the funding call on the Local Authorities Superannuation Fund Defined Benefits Plan. In 1998, state legislation governing the scheme was repealed and it became a 'regulated fund' under Commonwealth Government legislation, which introduced a requirement for it to be fully funded. Of the audited councils, Yarriambiack, Buloke and Towong's liability is the highest in real terms, and as a proportion of their rates revenue. Councils have adopted a range of different strategies to meet their liability. The impact of this shortfall highlights the vulnerability of small councils to unplanned events and their limited capacity to absorb this expenditure.

Support and guidance

It is important that appropriate support and guidance is provided to small councils to assist in addressing specific sustainability issues and improving the efficiency and effectiveness of council operations. This includes driving the adoption of better practices, improving their capability and providing targeted support or intervention when required.

While LGV does not have strategic priorities targeting the organisational sustainability of small councils, it provides a range of guidance and support broadly related to sustainability that is applicable to them. This includes developing and disseminating better practice guides that cover areas such as asset management, procurement and Best Value service delivery, delivering programs, and developing a performance management framework. However, there are opportunities to make this guidance and support more directly targeted to areas of challenge for small councils and to build their capability and resilience.

LGV conducts monitoring and reporting activities to identify councils at high risk of sustainability issues. It has advised the Minister for Local Government about these councils and implemented actions to address issues when they have become critical. LGV could more proactively target small councils with appropriate support and advice before their situation becomes critical. The development of LGV's local government performance management framework provides an opportunity to more closely monitor councils' sustainability and respond appropriately to support them on a timely basis.

Recommendations

- Councils should clearly identify and publicly report their sustainability challenges and associated strategies and actions, including how they will monitor, report and evaluate their effectiveness, using relevant and appropriate performance indicators.

- Yarriambiack Shire Council should develop a long-term financial plan and all councils should update their existing plans in accordance with better practice.

- Councils should review service planning and delivery in accordance with Best Value Principles as a priority, including:

- assessing overall service delivery levels to determine appropriate levels and provide the rationale for their decision

- consulting with their communities on their ability and willingness to pay for desired services in the development of the council plan

- developing a plan to regularly review all services over time.

The Department of Planning and Community Development should:

- review and update its asset management guidance

- consider making the development of a long-term financial plan mandatory and provide support and guidance in the development of these

- routinely review the guidance and support it provides so that it is aligned with areas of highest need and addresses gaps in councils' capability and capacity

- expedite implementation of the planned local government performance reporting framework and make sure it includes appropriate sustainability indicators.

Submissions and comments received

In addition to progressive engagement during the course of the audit, in accordance with section 16(3) of the Audit Act 1994 a copy of this report, or relevant extracts from the report, was provided to the Department of Planning and Community Development and to the following five councils, with a request for submissions or comments:

- Buloke Shire Council

- Golden Plains Shire Council

- Strathbogie Shire Council

- Towong Shire Council

- Yarriambiack Shire Council.

Agency views have been considered in reaching our audit conclusions and are represented to the extent relevant and warranted in preparing this report. Their full section 16(3) submissions and comments are included in Appendix B.

1 Background

1.1 Small councils

There are 79 local governments in Victoria. Of these, 21 are classified as small councils with populations of less than 20 000 people. These councils are located in rural areas and administer 89 893 square kilometres, or 40 per cent of Victoria's total area, and serve 217 000 people—4 per cent of the population.

Figure 1A shows the location of the 21 small councils in Victoria with the five audited councils highlighted.

Figure 1A

Location of 21 small councils

Source: Victorian Auditor-General's Office.

1.1.2 Small council funding

Small councils are heavily dependent on government grants to continue operating. In 2011–12, small councils generated operating revenue of $701 million, with government grants accounting for $360 million, or 51 per cent, and rates and charges contributing $216 million or 31 per cent. In contrast, government grants account for around 22 per cent and rates around 49 per cent of total revenue across all 79 councils.

1.1.3 Organisational sustainability of small councils

Organisational sustainability means that councils have the capacity to function efficiently, effectively and economically to meet the current and future needs of their communities to an acceptable standard. Core attributes of organisational sustainability include:

- sound governance to guide effective delivery of council activities

- effective planning to support current and future council operations

- sound financial management to meet current and future financial commitments

- optimum use of available resources

- use of community engagement to enable prioritisation of services and asset management according to community needs

- effective workforce planning and management.

Small councils face a range of issues and challenges that impact organisational sustainability, some of which may be outside of their control. These include:

- population decline and demographic changes such as ageing populations

- their location within regions including proximity to large regional towns

- recruiting and retaining qualified or skilled staff

- large networks of roads and other infrastructure to maintain

- increasing service delivery costs and servicing large geographic areas

- dealing with major unplanned events, such as the recent defined benefits superannuation shortfall, where the extent of liability was unknown.

1.2 Legislation and better practice

Local Government Act 1989

The Local Government Act 1989 (the Act) stipulates the primary objective of a council is to endeavour to achieve the best outcomes for the local community, having regard to the long term and cumulative effects of decisions. In seeking to achieve its primary legislative objective, a council must have regard to the following facilitating objectives:

- to promote the social, economic and environmental viability and sustainability of the municipal district

- to ensure that resources are used efficiently and effectively, and services are provided in accordance with the Best Value Principles to best meet the needs of the local community

- to improve the overall quality of life of people in the local community

- to promote appropriate business and employment opportunities

- to ensure that services and facilities provided by the council are accessible and equitable

- to ensure the equitable imposition of rates and charges

- to ensure transparency and accountability in council decision-making.

Under the Act, councils are required to develop planning and accountability reports, and apply sound financial management and Best Value Principles, as shown in Figure 1B.

Figure 1B

Local Government Act 1989 requirements

|

Planning and accountability reports |

|---|

|

(a) Council Plan including the strategic objectives, strategies for at least the next four years and strategic indicators (b) Strategic Resource Plan setting out the required financial and non-financial resources for at least the next four years to achieve the strategic objectives (c) Budget containing a description of the activities and initiatives to be funded and how they will contribute to achieving the strategic objectives (d) Annual Report containing a report of its operations during the financial year, audited standard and financial statements for the financial year. |

|

Sound financial management principles |

|

A council must: (a) manage financial risks faced by the council (b) pursue spending and rating policies consistent with a reasonable degree of stability in the level of the rates burden (c) ensure that decisions are made and actions are taken having regard to their financial effects on future generations (d) ensure full, accurate and timely disclosure of financial information. |

|

Best Value Principles |

|

(a) All services must meet the quality and cost standards (b) All services must be responsive to the needs of its community (c) Each service must be accessible to those whom the service is intended for (d) A council must achieve continuous improvement in the provision of services for its community (e) A council must develop a program of regular consultation with its community (f) A council must report regularly to its community on its achievement in relation to the principles set out above. |

Source: Victorian Auditor General's Office based on information from the Local Government Act 1989.

Better practice and sector guidance

Better practice guidance material and other support is available to councils from a range of sources. This includes material developed by Local Government Victoria (LGV), the Municipal Association of Victoria (MAV), Victorian Local Governance Association (VLGA), Local Government Professionals (LGPro) and organisations such as the Institute of Public Works Engineering Australia (IPWEA) and the Australian Centre of Excellence for Local Government (ACELG). Key better practice guidance material is set out in Figure 1C.

Figure 1C

Better practice guidance material

|

Title |

Description |

Published by |

|---|---|---|

|

Local Government Planning and Reporting Better Practice Guide (2013) |

A guide to assist councils to meet statutory planning and accountability requirements, including guidance in the development of the council plan and reporting performance |

LGV |

|

Long-term Financial Planning (2012) |

Developed to assist organisations that are involved in service delivery and long-term asset management in preparing a long-term financial plan |

IPWEA and ACELG |

|

Asset Management Policy, Strategy and Plan (2004) |

Guidelines for developing an asset management policy, strategy and plan |

LGV |

|

'STEP' asset management improvement program (since 2003) |

A program for councils covering asset management and planning as essential for effective delivery of services |

MAV |

|

Victorian Local Government Best Practice Procurement Guidelines 2013 |

Guidelines for dealing with the procurement cycle (planning, implementation, management and performance evaluation), reporting on procurement and meeting obligations under the Act |

LGV |

|

Embedding Community Priorities into Council Planning (2008) |

A set of guidelines for involving the community in development of the council plan |

LGPro |

|

A guide to achieving a whole of organisation approach to Best Value (2006) |

Designed to assist in developing or enhancing formal or informal improvement and planning frameworks to effectively incorporate the Best Value Principles |

LGV developed in partnership with LGPro Corporate Planner's Network and the Best Value Commission |

Source: Victorian Auditor-General's Office.

1.3 Roles and responsibilities

1.3.1 Local Government Victoria

LGV, a division of the Department of Planning and Community Development (DPCD), supports and advises the Minister for Local Government in administering the Act. The role of LGV also includes overseeing, supporting and encouraging local government and providing advice and support to councils in relation to their roles and responsibilities under the Act. LGV also works in partnership with the local government sector and other parts of government to improve and reform business, governance and funding practices to maximise value and accountability.

1.3.2 Local councils

Councils deliver a wide range of services to their communities including child and family day care services, meals on wheels, waste collection, planning and recreational services. Councils also build and maintain community assets and infrastructure, including roads, footpaths and drains, and enforce various laws. Councils are required by the Act to promote the sustainability of the municipal district and to ensure effective and efficient use of resources. Councils are also expected to provide services in accordance with Best Value Principles to best meet the needs of the local community.

1.3.3 Victoria Grants Commission

The Victoria Grants Commission's primary function is to allocate revenue provided by the Commonwealth Government to municipal councils in Victoria according to the Local Government (Financial Assistance) Act 1995 and a set of national distribution principles. All funds allocated by the Commonwealth are distributed to councils. The commission is funded by the Victorian Government through DPCD.

1.4 Previous audits

1.4.1 Local Government: Results of the 2011–12 Audits

VAGO's Local Government: Results of 2011–12 Audits report presents the results of our financial audits of 103 entities within the local government sector, including Victoria's 79 councils. It provides a detailed analysis of council financial reporting, performance reporting, financial results, financial sustainability and internal controls. It analyses trends in six key financial sustainability indicators (underlying result, liquidity, self-financing, indebtedness, capital replacement and renewal gap), reflecting both short- and long-term sustainability, over a five-year period and includes forecasts over a three-year period.

1.4.2 Related performance audits

Other reports relating to organisational sustainability that VAGO has tabled over the past few years include:

- Ratings Practices in Local Government (February 2013)

- Business Planning for Major Capital Works and Recurrent Services in Local Government (September 2011)

- Fees and Charges—cost recovery by local government (April 2010).

1.5 Audit objective and scope

The objective of this audit was to assess the effectiveness of the planning and management undertaken by small councils to support their long-term organisational sustainability. It also assessed guidance and support provided by LGV and aimed to identify practices that could help drive improvements across the local government sector.

The audit focused on the following five selected councils:

- Buloke Shire Council

- Golden Plains Shire Council

- Strathbogie Shire Council

- Towong Shire Council

- Yarriambiack Shire Council.

It assessed whether they have:

- a sound understanding of the sustainability challenges and issues facing their council

- developed appropriate strategies that consider a range of options for addressing sustainability issues and challenges

- evaluated how effective sustainability strategies have been

- been provided with appropriate guidance and support to address sustainability issues by LGV.

1.6 Method and cost

The audit was conducted in accordance with section 15 of the Audit Act 1994 and Australian Auditing and Assurance Standards. Pursuant to section 20(3) of the Audit Act 1994, any persons named in this report are not the subject of adverse comment or opinion.

The cost of the audit was $385 000.

1.7 Structure of the report

The report is structured as follows:

- Part 2 examines the financial position of councils

- Part 3 discusses sustainability issues, challenges and strategies

- Part 4 examines support, guidance, monitoring and reporting undertaken by LGV.

2 Financial sustainability

At a glance

Background

To be financially sustainable, councils need to be able to meet their current and future expenditure requirements. They also need to be able to absorb foreseeable changes and materialising risks, and manage the impact of their changing revenue and expenditure requirements. Assessing trends in key financial indicators provides insight into the risks to small councils' financial sustainability.

Conclusion

In 2011–12, Buloke had high-risk, immediate to shorter-term sustainability concerns, while the remaining four audited councils were classed as having a low risk. However, several councils are projected to have deteriorating positions against key financial indicators, which places them at an increased risk of short-term and immediate sustainability concerns.

Over the past five years, the reliance of the audited councils on government grants has increased substantially. While councils have increased the amount of own-source revenue they generate through rates and user charges, it has not been enough to keep pace with their increased costs. Given current Commonwealth and State Budget positions and the economic climate, the audited councils' increasing reliance on grants may expose them to significant financial risk if the number and value of grants are reduced.

Findings

- On average, government grants have increased significantly as a proportion of total revenue over the past five years across all of the audited councils.

- In 2012, a superannuation defined benefits plan funding shortfall had a significant impact on employee expenses for all of the audited councils.

- Councils have generally not reviewed whether there is scope to introduce or increase user fees and charges.

2.1 Introduction

To be financially sustainable, councils need to be able to meet current and future expenditure as it falls due. They also need the ability to absorb foreseeable changes and materialising risks without significantly changing their revenue and expenditure policies.

Financial sustainability should be viewed from both short- and long-term perspectives. Short-term indicators relate to the ability of a council to maintain positive operating cash flows in the near future, or the ability to generate an operating surplus in the next financial year. Long-term indicators focus on strategic issues such as the ability to fund significant asset replacement or reduce long-term debt. Councils are unlikely to remain viable without effective expenditure management and revenue maximisation practices to underpin long-term organisational sustainability.

An assessment of trends in key financial indicators, based on councils' projections, provides insight into the risks to small councils' financial sustainability that may warrant attention. Similarly, examining trends in the composition of revenue and expenditure highlights potential issues and risks with particular patterns of revenue and expenditure for high-risk councils.

2.2 Conclusion

Over the past five years, the reliance of audited councils on government grants has increased substantially. While rates and charges have increased in real terms, they have decreased as a proportion of revenue over the same period, and this increase in rates and charges has not been enough to keep pace with councils' increase in costs.

In 2011–12, Buloke had high-risk, immediate to shorter-term sustainability concerns, while the remaining four audited councils were classed as having low risk of financial sustainability concerns. However, several councils are projected to have deteriorating positions against key financial indicators, which places them at an increased risk of short-term and immediate sustainability concerns.

Given current Commonwealth and State Budget positions and the economic climate, the audited councils' increasing reliance on grants may expose them to significant financial risk if the number and value of grants are reduced.

2.3 Councils' financial sustainability

2.3.1 Current and future trends

VAGO's six key financial sustainability indicators, which reflect short-and long-term sustainability over the past five years, provide an insight into the financial sustainability of councils. The indicators are:

- underlying result—councils generate enough revenue to cover operating costs, including the cost of replacing assets reflected in depreciation expense

- liquidity—councils have sufficient working capital to meet short-term commitments

- self-financing—councils generate sufficient operating cash flows to invest in asset renewal and repay any debt that may have been incurred in the past

- indebtedness—councils do not overly rely on debt to fund capital programs

- capital replacement—councils replace assets at a rate consistent with their consumption

- renewal gap—councils maintaining existing assets at a consistent rate.

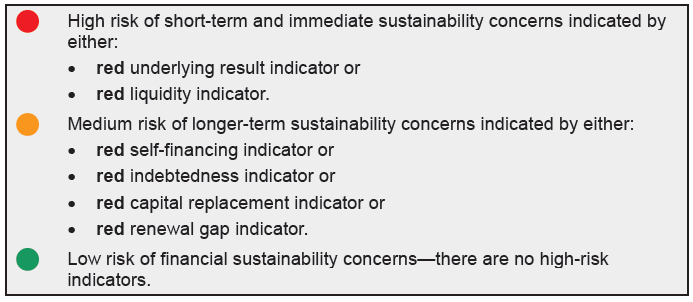

Appendix A describes the sustainability indicators in more detail, including the risk assessment criteria and the significance of these. The indicators are used to evaluate each council and provide a financial sustainability risk assessment. A high risk of short‑term and immediate financial sustainability concerns is indicated by either a high‑risk underlying result or liquidity indicator. A medium risk of longer-term financial sustainability concerns is indicated by a high-risk assessment for either of the remaining four indicators—self-financing, indebtedness, capital replacement and renewal gap. A low risk of financial sustainability concerns means there are no high‑risk indicators.

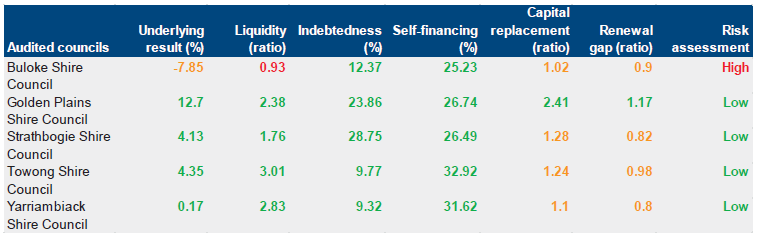

VAGO's Local Government: Results of the 2011–12 Audits report presents the results of financial audits of Victoria's 79 councils based on the six financial sustainability indicators. Figure 2A shows the results for the audited councils.

Figure 2A

Financial sustainability risk assessment results, 2011–12

Source: Victorian Auditor-General's Office.

Figure 2A shows that as at 30 June 2012 Buloke had a high risk of short-term and immediate sustainability concerns. This is highlighted by indicators suggesting it has a risk of long-term run-down to cash reserves, inability to fund asset renewals (underlying result) and insufficient current assets to cover current liabilities (liquidity). The remaining four councils in the audit were classed as having a low risk of financial sustainability concerns in 2011–12.

The Minister for Local Government appointed an Inspector of Municipal Administration (the Inspector) to independently assess Buloke's financial health in response to VAGO's qualification of its financial accounts in 2010–11—this is discussed further in Part 4.4. A qualification means that the financial report is materially different to the requirements of the relevant reporting framework or accounting standards, and is less reliable and useful as an accountability document.

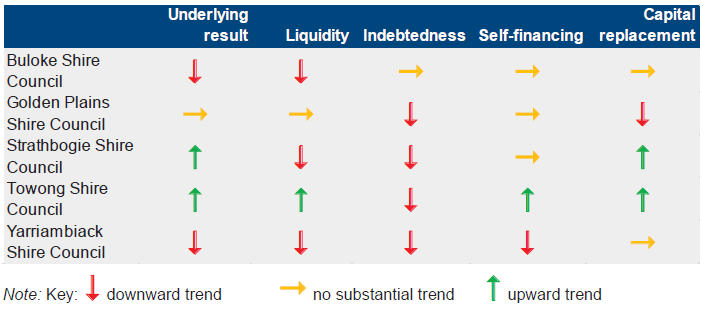

Figure 2B shows the projected trend for five of the six indicators, based on councils' budget projections, for the period 2012–13 to 2014–15. Projected data is not available for the renewal gap indicator.

Figure 2B

Financial sustainability indicator projections, 2012–13 to 2014–15

Source: Victorian Auditor-General's Office.

Buloke's underlying result and liquidity is projected to deteriorate over the next three years and it is expected to remain at high risk of short-term and immediate sustainability concerns. Its underlying result improves in 2012–13 due to forecast capital grants from the Natural Disaster Recovery Fund, but it is projected to return to a worse-than-current position by 2015. Other audited councils also show deteriorating results against some indicators over the next three years.

The results suggest Yarriambiack is at risk of potential short-term and immediate financial sustainability concerns due to the deteriorating position of its underlying result and liquidity indicators, while it also has deteriorating indebtedness and self-financing indicators. Similarly, Strathbogie has a deteriorating liquidity indicator, but its underlying result is projected to improve. Its indebtedness indicator is also projected to deteriorate, however, its underlying result and capital replacement indicators are projected to improve.

Golden Plains' capital replacement and indebtedness indicators are projected to deteriorate. Towong's indebtedness indicator is also projected to deteriorate, although its other indicators are projected to improve. The deteriorating indicators for Golden Plains and Towong suggest they are at increased risk of longer-term sustainability concerns if these indicators became high risk.

2.3.2 Council revenue

Councils generate revenue directly from rates, user fees and a range of charges—known as own-source revenue—and from other sources such as state and Commonwealth Government grants and developer contributions. The main types of revenue are:

- Rates and other charges—property taxes including general rates, the municipal charge, service rates or charges, and special rates or charges.

- User fees and charges—fees and charges for compulsory services, such as statutory planning fees, or discretionary services, such as recreation services, child care or applications for planning and building permits.

- Contributions—payments or in-kind works, facilities or services provided by developers towards the supply of infrastructure such as roads, storm water run‑off management systems, open space and community facilities required to meet the future needs of local residents in new land developments.

- Grants—financial assistance grants provided by the Commonwealth or state governments. The Commonwealth Government provides general purpose and local roads grants, and councils may also receive grants following natural disasters or other emergency events. The Department of Planning and Community Development administers a range of state government grant programs available to local governments, such as community facility funding, community works grants, country football and netball facilities grants, fire ready community grants and library infrastructure grants.

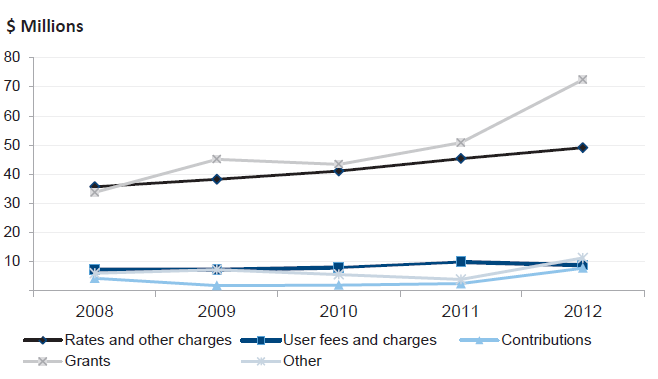

- Figure 2C shows the revenue raised from key sources for the period 2007–08 to 2011–12.

Figure 2C

Total revenue for the five councils

Source: Victorian Auditor-General's Office.

While Figure 2C shows that the amount of grants and rates and charges have increased, grants are the main source of revenue that is increasing as a proportion of total revenue. Figure 2D shows that on average councils' rates and charges, and user fees and charges have decreased as a proportion of total revenue. This implies an increasing reliance on grants to fund expenditure requirements compared to other revenue sources, which is concerning given the current Commonwealth and State Budget positions and economic climate.

Figure 2D

Revenue sources for the five councils as a percentage of total revenue, 2008 to 2012

|

Rates and other charges (%) |

User fees and charges (%) |

Contributions (%) |

Grants (%) |

Other (%) |

|

|---|---|---|---|---|---|

|

2008 |

41.0 |

8.3 |

5.0 |

38.7 |

6.9 |

|

2009 |

38.4 |

7.3 |

1.9 |

45.2 |

7.3 |

|

2010 |

41.1 |

8.0 |

2.0 |

43.4 |

5.6 |

|

2011 |

40.3 |

8.8 |

2.2 |

45.2 |

3.5 |

|

2012 |

32.8 |

5.9 |

5.2 |

48.5 |

7.6 |

|

Average rate of change per year |

–1.4 |

–0.3 |

0.1 |

1.9 |

–0.3 |

Source: Victorian Auditor-General's Office.

The amount of grants for the audited councils has more than doubled over five years from $33.766 million in 2007–08 to $72.434 million in 2011–12. This equates to an average increase of 25 per cent per year. The increase in grants as a proportion of total revenue averaged 1.9 per cent a year. Over the same period, rates and charges and user fees and charges increased from $35.714 million to $49.083 million and $7.275 million to $8.810 million respectively, but councils' reliance on these has declined over the same period by 1.4 per cent and 0.3 per cent per annum respectively. This means that despite increases in real terms, councils' own-source revenue has decreased proportionally by an average of 1.7 per cent per year.

Therefore, while councils have increased the amount of own-source revenue they generate through rates and user charges, it has not been enough to keep pace with their increase in costs. Despite all five audited councils having committed to maintaining existing service levels, there is limited evidence that they have comprehensively reviewed their services or service levels. Councils have generally not reviewed whether there is scope to introduce, or increase user fees and charges to at least partially address their revenue requirements. Golden Plains advised it conducted a review of user fees and charges during the 2012–13 budget process, and that an outcome of the review was to increase non-statutory fees by 9.5 per cent. However, it was unable to provide documentary evidence of this review to show the analysis and rationale underpinning the decision to increase fees.

2.3.3 Council expenditure

Councils have a range of operating expenses, including the following key expenses:

- employee benefits—includes wages and salaries, leave entitlements, redundancy payments and superannuation contributions

- contract payments—includes payments for services delivered by contractors, such as waste collection or parks and gardens maintenance, and council staff positions that are filled by contractors

- depreciation—the systematic allocation of a fixed asset's capital value as an expense over its expected useful life to take account of normal usage, obsolescence, or the passage of time

- borrowing costs—costs such as interest associated with borrowings taken out to fund council expenditure.

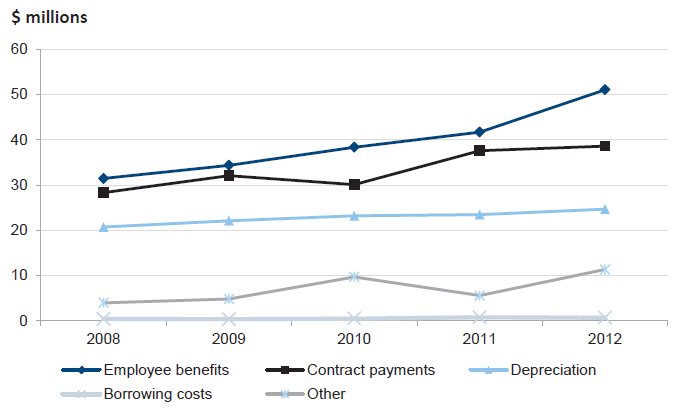

Figure 2E shows the trend in key expenses for the period 2007–08 to 2011–12.

Figure 2E

Total expenses for the five councils

Note: 'Other' includes a range of expenses such as travel costs and printing.

Source: Victorian Auditor-General's Office.

Figure 2F shows the councils' key expenses over the period 2007–08 to 2011–12 as a proportion of total expenses.

Figure 2F

Expenses for the five councils as a percentage of total expenditure, 2008 to 2012

|

Employee benefits (%) |

Contract payments (%) |

Depreciation (%) |

Borrowing costs (%) |

Other (%) |

|

|---|---|---|---|---|---|

|

2008 |

37.0 |

33.4 |

24.4 |

0.5 |

4.7 |

|

2009 |

36.7 |

34.2 |

23.6 |

0.4 |

5.1 |

|

2010 |

37.7 |

29.6 |

22.8 |

0.5 |

9.5 |

|

2011 |

38.2 |

34.5 |

21.5 |

0.7 |

5.1 |

|

2012 |

40.4 |

30.5 |

19.5 |

0.6 |

9.0 |

|

Average rate of change per year |

0.8 |

–0.5 |

–1.2 |

0 |

0.9 |

Source: Victorian Auditor-General's Office.

Overall, increasing expenses for the audited councils are largely being driven by higher employee benefits and contract payments. Employee benefits have risen from $31.429 million in 2008 to $51.053 million in 2012, which represents an average increase of 0.8 per cent per year as a proportion of total expenses. Advice from LGV to government suggests that local government recurrent expenditure has increased by more than twice the rate of inflation over the past decade, and aggregate expenditure on salaries and wages has increased by almost three times the national average in public sector wages and salaries over the same period.

The sharper increase in employee benefit expenses in 2012 is due to the funding call on the Local Authorities Superannuation Fund Defined Benefits Plan. In 1998, state legislation governing the scheme was repealed and it became a 'regulated fund' under Commonwealth Government legislation, which introduced a requirement for it to be fully funded. Of the audited councils, Buloke, Towong and Yarriambiack's liability is the highest in real terms and as a proportion of their rates revenue. The funding liability will have an impact on councils' liquidity, and may worsen this indicator. Councils have adopted a range of different strategies to meet their liability—these are discussed in section 3.3.6.

Contract payments, such as waste collection services, increased from $28.293 million in 2008 to $38.375 million in 2012, but decreased in terms of the proportion of total expenses by an average of 0.5 per cent per year. There was no change in borrowing costs as a proportion of total expenses. Depreciation expenses decreased as a proportion of total expenses, however, this is due to other expenses such as employee benefits increasing by a much greater amount. In real terms depreciation expenses increased fairly uniformly, by an average of 4.5 per cent per year. While there have been some changes with regard to how much key expenses represent in terms of overall expenses—particularly the increase in employee benefits—the mix of different expense categories has remained relatively stable over the past five years.

Given the risks to the audited councils' financial sustainability, it is essential that they effectively plan their long-term financial management and their management of assets. They should also efficiently and effectively deliver services and maximise the revenue they generate from service delivery so that this contributes to meeting their revenue requirements. These elements are discussed further in Part 3.

3 Sustainability issues, challenges and strategies

At a glance

Background

Small councils should have a sound understanding of their sustainability issues and challenges and develop appropriate strategies to address these and mitigate their impact as far as possible. They should also have effective long-term planning and asset management, deliver services effectively and efficiently and position themselves to remain viable in the medium- to long-term.

Conclusion

The audited councils generally have a sound understanding of sustainability issues and challenges and have implemented a range of strategies to address them. However, in some instances actions do not address the core problem. Councils generally cannot demonstrate the effectiveness of strategies or actions and whether these are having a material impact on improving their sustainability. There is scope to improve in financial, asset and service planning and management, and to better link actions to sustainability challenges and outcomes.

Findings

- Audited councils generally face common sustainability issues and challenges.

- All councils except Yarriambiack have recently developed long-term financial plans, but these vary in quality and are not sufficiently integrated with asset management.

- Councils cannot demonstrate that service delivery is efficient and effective.

Recommendations

- Councils should clearly identify and publicly report their sustainability challenges and actions, and how they will monitor, evaluate and report on their effectiveness.

- Yarriambiack Shire Council should develop a long-term financial plan and all councils should update their existing plans in accordance with better practice.

- Councils should review service planning and delivery as a priority.

3.1 Introduction

Small councils face a number of issues and challenges that impact organisational sustainability. They should have a sound understanding of the particular issues and challenges impacting their sustainability and develop appropriate strategies to address these to mitigate their impact as much as possible.

It is important that small councils' operations are underpinned by effective financial planning and asset management, and effective and efficient service delivery. Councils also need to be vigilant in monitoring risks and factors likely to significantly affect sustainability. This may not in itself provide assurance that a council will be sustainable; however, it will position councils better to remain viable in the medium to long term.

3.2 Conclusion

The audited councils generally have a sound understanding of the sustainability issues and challenges they face. However, it is not evident that all of their strategies and actions are effectively addressing the identified issues. While some council strategies are supported by analysis and are well informed, other responses have been reactive and are not underpinned by a strategy that addresses the core problem.

While councils have made some efforts to improve planning for long-term financial sustainability, managing assets, and delivering services effectively and efficiently, further work is required in these areas. Four of the five councils have developed long‑term financial plans; however, these vary in quality and are not adequately integrated with asset management plans. Councils generally do not plan or deliver services in accordance with Best Value Principles and cannot demonstrate they are delivering services efficiently and effectively. Consequently, councils cannot demonstrate they are operating as efficiently and effectively as possible.

3.3 Organisational sustainability challenges, issues and planning

Councils should have a sound understanding of the sustainability challenges and issues they face, and develop and implement strategies to address these. Issues and challenges are generally identified in council plans, strategic resource plans, annual reports, annual budgets and rating strategies. There are a number of common sustainability issues and challenges across the audited councils, including:

- having effective financial planning and asset management

- effectively and efficiently delivering services

- recruiting and retaining qualified and skilled staff

- dealing with the impact of population ageing and/or population changes

- dealing with the defined benefits superannuation shortfall.

3.3.1 Long-term financial planning

Effective long-term financial planning is crucial to sustainability and is particularly important for councils that are responsible for managing and generating service from a large stock of long-lived assets relative to their annual income. Councils need to deliver services that meet community needs in a financially sustainable manner, and plan for the needs of current and future generations. In the past, councils have relied on a short-term financial planning horizon, which was essentially limited to the annual budget processes. This approach limits councils' ability to adequately plan for their long-term financial sustainability.

Better practice

A long-term financial plan expresses in financial terms the activities and level of services that a council proposes to undertake or provide over the short, medium and long term to achieve the objectives in its council plan. It should guide future strategies and confirm that the council can remain financially sustainable.

It is not mandatory in Victoria for councils to develop a long-term financial plan and there is no existing statewide guidance to assist councils. However, in January 2012 the Commonwealth Government released a better practice guide (Institute of Public Works Engineering Australia Practice Note No. 6 – Long-Term Financial Planning – Version 1.0, January 2012). Based on this guide, a long-term financial plan:

- is a high-level document that can be easily understood by the community, rather than a series of complex spread sheets—although councils may develop these for internal use

- includes a brief narrative overview to help the reader understand the purpose of the plan, the basis of its preparation and the key conclusions that can be drawn from the financial data

- has robust and reliable financial data at a summary level based on accrual accounting financial statements, including projected income and expenditure, balance sheet and cash flow statement—accrual accounting is important for financial sustainability since it measures the performance and position of a council by recognising economic events regardless of when cash transactions occur to give a more accurate picture of the current financial condition

- has a clear financial strategy on which the plan is based, such as a rating strategy and borrowing strategy, for achievement of financial sustainability

- has a small number of key performance indicators for measuring financial sustainability that are relevant and appropriate—a relevant indicator has a logical and consistent relationship with the plan's objectives and an appropriate indicator is one that is underpinned by sufficient information to assess its achievement against objectives, outcomes and outputs—and include targets that are clearly linked to objectives

- has a sensitivity analysis that highlights key factors most likely to materially impact on the achievement of the plan's financial targets, such as anticipating a significantly high level of population growth in its area which may affect operating revenue and expenses

- is integrated with a council's asset management and capital works statement—see Section 3.3.2 Asset management planning

- is reviewed and updated at least annually

- is publicly reported.

Assessment of current plans

Golden Plains developed a long-term financial plan in 2006, while Buloke, Strathbogie and Towong developed their plans in the past two years. Yarriambiack has committed to developing a long-term financial plan in its last three annual budgets, but has not yet done so. While Yarriambiack advised that it prepares 10 years of financial projections as part of the development of its strategic resource plan, these do not contain the key elements of a long-term financial plan. Yarriambiack advised that it plans to engage an external party to develop a long-term financial plan.

Figure 3A summarises our assessment of existing council long-term financial plans against key attributes from the Commonwealth Government better practice guide, which sets out the recommended elements of a long-term financial plan.

Figure 3A

Assessment of long-term financial plans against better practice

|

Key attribute |

Council |

||||

|---|---|---|---|---|---|

|

Buloke |

Golden Plains |

Strathbogie |

Towong |

||

|

Plan developed |

2011 |

2006 |

2011 |

2012 |

|

|

Time period covered |

10 years |

10 years |

10 years |

10 years |

|

|

High-level document |

Yes |

Yes |

Yes |

No |

|

|

Brief narrative overview |

Yes |

Yes |

Yes |

No |

|

|

Financial data |

Yes |

Not cash flow |

Yes |

Yes |

|

|

Financial strategy |

Yes |

Yes |

Yes |

No |

|

|

Performance indicators for measuring financial sustainability |

Yes |

Yes |

Yes |

No |

|

|

Relevant and appropriate |

No |

No |

Yes |

n.a. |

|

|

Clear targets |

No |

No |

Partially |

n.a. |

|

|

Small in number |

No |

Yes |

Yes |

n.a. |

|

|

Sensitivity analysis |

No |

No |

No |

No |

|

|

Reviewed at least annually |

Yes |

n.a. |

Yes |

Yes |

|

|

Publicly reported |

Yes |

Yes |

Yes |

Partially |

|

Source: Victorian Auditor-General's Office.

Golden Plains and Strathbogie's plans are high-level, stand-alone documents that are publicly available, while Buloke's plan is incorporated into the council's strategic resource plan. Towong's plan consists of a series of spread sheets and, while four years of financial projections from the plan were reported in its strategic resource plan in the annual budget, the rest of the plan is not publicly available.

All of the plans contain the recommended financial data at a summary level based on accrual accounting financial statements, except Golden Plains which does not include a cash flow statement. Without this, it is difficult to measure some performance indicators, such as cash balance and discretionary retained earnings.

Buloke, Golden Plains and Strathbogie's indicators measure factors that define financial sustainability; including, operating surplus and underlying result. However, only Strathbogie's indicators are relevant and appropriate as they have a logical and consistent relationship with the plan's objectives. Strathbogie's is also the only plan that contains clear targets against indicators—such as those for asset renewal investment and borrowings—although it does this for only two of the six indicators. Buloke uses a large number of indicators, which could make it difficult for decision‑makers and stakeholders to interpret results and gain a clear understanding of outcomes or the council's position.

It is important that monitoring, evaluation and reporting of performance indicators is conducted routinely and remedial action is taken where performance targets or expected results are not achieved. Most of these plans have only recently been developed, so it is too early to say whether councils are doing this. The plans do not provide any information about whether the councils propose to review and/or report publicly on these indicators and if so, how often.

All of the councils have reviewed and updated their plans at least annually. However, they have not explained in their plans what, if any, changes have been made from the review process. For example, Buloke deleted, without explanation, one of the 2011‑12 plan's objectives to 'achieve a break even operating result within five years'. Buloke has advised that this objective was removed due to substantial costs relating to flood recovery impacting on the council's ability to achieve it. However, removing the objective without providing an explanation reduces transparency and does not represent good practice in performance monitoring and reporting.

While the plans, particularly Strathbogie's, reflect a number of better practice elements, work is needed by all councils to address deficiencies, and effectively plan their finances from a long-term perspective to support their sustainability.

3.3.2 Asset management planning

Effective asset management planning is also crucial to long-term sustainability. Councils' infrastructure assets represent a vast investment that has been built up over many generations and includes roads, bridges, drainage, buildings, parks and recreational facilities. Assets are acquired for their service delivery potential, so service delivery needs should form the basis of all asset management practices and decisions.

Robust asset management planning is required for councils to effectively manage their significant stock of assets. This planning is necessary to guide the scheduling of maintenance, refurbishment, renewal and replacement of assets and to achieve specific service levels, while minimising asset life cycle costs. Asset management plans should also set out expenditure projections as input for the long-term financial plan. Councils have more than one asset management plan because they generally develop separate plans to cover each major asset class.

A standard statement of capital works sets out actual against planned capital expenditure that relates to larger assets, including property, plant and equipment.

Current status

All of the audited councils had asset management policies, strategies and plans, and have made efforts to improve asset management through training and support programs, such as participation in the Municipal Association of Victoria's Asset Management Improvement 'STEP' program. As part of this program, each council completed self-assessments of their asset and financial management, and used these to develop a prioritised improvement plan. These assessments indicate that there is still scope for improvement, particularly in relation to asset management plans.

Integration with long-term financial plans

It is important that asset management plans and capital works statements are appropriately integrated with long-term financial plans so that these needs are adequately considered in financial planning. Of the four councils with long-term financial plans, each committed in their asset management policy or strategy to integrate their asset management plans with their long-term financial plans.

A key aspect of integrating asset and financial planning is for councils to develop 10‑year expenditure projections in asset management plans and then use these to populate the capital works statements in the long-term financial plan. While all long‑term financial plans contain a capital works statement, which covers material assets and their expenditure forecasts over the next 10 years, none of the asset management plans contain up-to-date 10-year expenditure forecasts. Councils' asset management plans either contain out-of-date figures (Buloke and Strathbogie), short-term projections (Golden Plains), and/or plans are still under development (Towong, Golden Plains and Strathbogie). This provides limited assurance that each council's asset management requirements were appropriately considered in developing the figures in the capital works statements. However, Buloke has advised that its plans have not been updated due to uncertainty related to the timing of funding for flood recovery.

3.3.3 Efficient and effective service delivery

Councils deliver a wide range of services to their communities. Some local government service delivery is mandated or unavoidable—for example, statutory obligations—while some is essentially discretionary to meet the needs of communities, such as providing swimming pools and family day care. Even within the context of necessary expenditures, there is scope to decide what the appropriate nature of the service and service levels should be.

Service reviews

The Local Government Act 1989 requires councils to provide services in accordance with the Best Value Principles, which include considering service cost and quality standards, value for money, and community expectations and values. The principles also call for balance between affordability and accessibility of services.

Councils should conduct regular service reviews in accordance with the Best Value Principles to assess the effectiveness and efficiency of their services, and to take action where necessary so that their services continue to meet the community's needs and prevent creating an unnecessary impost if inefficient.

Other than narrow reviews of specific services, such as to identify cost savings, none of the audited councils have undertaken comprehensive reviews of the services they provide in accordance with Best Value Principles. They have also not reviewed service levels to assess the effectiveness and efficiency of service delivery. This provides limited assurance that expenditure on service delivery is informed by an adequate understanding of community needs or the effectiveness and efficiency of council services. Nevertheless, all councils have committed to maintaining existing services and the independent review of Buloke's finances found that the council's commitment to maintaining existing service levels was unsustainable.

Only Towong has completed a service review based on the Best Value Principles, but this was only for one service—the councils' records management service. This review was facilitated by LGV in June 2012 in connection with the Local Government Reform Fund and was part of the Building Best Value Capacity Project in collaboration with four other councils—Alpine, Campaspe, Indigo and Moira. This is discussed further in Part 4.3.

Other reviews by the audited councils have been primarily limited to cost analysis and do not constitute a comprehensive service review in accordance with Best Value Principles. Examples of the reviews conducted include:

- Towong recently secured funding from the state government through the Sustainability Fund for a Demand Reduction Program that is currently being undertaken with Indigo Shire Council. This aims to achieve environmental and efficiency savings of $250 000 per year and such a program could be replicated across other councils.

- Buloke has conducted a number of reviews of services to identify cost savings. In response to recommendations from the Inspector of Municipal Administration's review, it has committed to undertaking a comprehensive analysis of services, which it suggests will be progressively implemented as resources allow. This is based on the Inspector's finding that it is financially unsustainable to maintain existing service levels. Work will include a cost-benefit analysis of discretionary services to determine which should be ceased, deferred or continued.

Consulting with the community about service delivery

Councils use a variety of mechanisms to engage with their communities to provide feedback on services and projects. However, the community consultation that occurs tends to be related to new projects, infrastructure or proposed services that councils plan to deliver, or to seek feedback on the draft council plan. Councils could not demonstrate they had adequately sought, considered and analysed community needs in relation to council services when initially formulating their council plans.

Better consultation with communities on their ability and willingness to pay for both existing and new services and assets when developing council plans could be used to assess overall service delivery levels. This could help councils to determine required levels and to prioritise the delivery of services appropriate to the needs of communities. The current approach provides limited assurance that council plans adequately reflect residents' needs as the community is not involved in the initial development.

Strathbogie is currently conducting community consultation to inform the development of its council plan, which includes conducting a survey that asks respondents to rank council services in importance. However, it is too early to assess the effectiveness of this in prioritising services and informing overall service levels.

Shared services

All audited councils participate in shared services with either neighbouring councils or other organisations in their region. This includes both internal operational activities and the delivery of council services. These arrangements generally involve sharing a component of the activity or service, such as information sharing to plan services, or sharing a resource, rather than the full delivery of a service. The main current and proposed shared services arrangements and the councils participating in them are shown in Figure 3B.

Figure 3B

Main types of shared services at audited councils

|

Shared service |

Councils |

||||

|---|---|---|---|---|---|

|

Buloke |

Golden Plains |

Strathbogie |

Towong |

Yarriambiack |

|

|

Operational activities |

|||||

|

Business improvement |

Yes |

||||

|

ICT |

Yes |

Yes |

|||

|

Payroll |

Yes |

Proposed |

|||

|

Procurement |

Yes |

Yes |

|||

|

Council services |

|||||

|

Aged and disability |

Yes |

Yes |

|||

|

Building services |

Yes |

Proposed |

|||

|

Child/family/youth |

Yes |

Yes |

|||

|

Environment |

Yes |

Yes |

|||

|

Emergency management |

Yes |

Yes |

Yes |

||

|

Health |

Yes |

Yes |

Yes |

||

|

Library |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Roads |

Yes |

Yes |

Yes |

||

|

Transport |

Yes |

Yes |

Yes |

||

Note: Some councils also use the same contractor to deliver services, but not through a formal arrangement and this is not considered a shared service. These types of arrangements are not included in the table.

Source: Victorian Auditor-General's Office based on information from audited councils.

The necessary rationale for councils adopting shared services is generally not clearly documented and is therefore difficult to assess. Although it is reasonable to expect there to be savings and efficiencies through sharing these activities, there have been no evaluations of the arrangements and so the extent of this is not known. Therefore, it is not clear that sharing these services is improving the sustainability of these councils. With some exceptions, such as libraries, these arrangements are not mature or undertaken on a large scale.

3.3.4 Recruiting and retaining qualified and skilled staff

Small councils in regional and rural areas can face challenges in attracting appropriately qualified and skilled staff and may also experience difficulty in retaining staff. A council's location within the region and its proximity to large regional towns can also affect this.

This can be a particular problem when positions that are hard to fill and have a high turnover are critical to service delivery and council operations.

The State Services Authority (SSA) has identified common challenges for the public sector located in rural and regional Victoria, which also apply to small councils, including:

- a low interest or even no response to particular job advertisements

- a reliance on people needing to relocate to take up critical roles

- prospective candidates being unfamiliar with their region or living in a regional and rural area

- negative perceptions of rural and regional living

- no local tertiary institutions supplying graduates with the required qualifications

- private and not-for-profit organisations offering more attractive remuneration or conditions

- partners of applicants or new staff needing to find work in the area

- limited accommodation for staff or few options that meet their expectations.

Strategies

Workforce planning is one strategy that may assist councils to identify workforce needs, the barriers to attracting and retaining staff, and approaches to address the problem. SSA's 2006 Workforce Planning Toolkit for small to medium sized Victorian public service organisations recommends that a workforce planning framework include the following six elements:

- workforce analysis—analyse the workforce against organisational direction, internal workforce characteristics and capabilities, external labour market and environmental factors

- forecast future needs— identify future business needs, scenarios and workforce characteristics and capabilities

- analyse gaps— identify and analyse the gaps between future workforce needs and current workforce profile

- develop strategies—develop integrated business and human resources strategies to address the gaps between current and future workforce needs

- implement strategies—invest in strategies and change management processes to address workforce planning issues

- monitor and evaluate—evaluate the effectiveness of strategies to determine success of planned changes and impact on business performance.

All audited councils except Yarriambiack identified recruiting and retaining appropriately qualified and skilled staff as an issue, and some councils have implemented strategies to address these problems.

Golden Plains developed a workforce plan in 2009. This plan contains a number of elements recommended by the SSA's guide, including a workforce analysis, forecast of future needs, analysis of gaps and development of strategies. These strategies include succession planning for high priority positions, flexible employment arrangements, and working with regional universities to identify engineering students interested in a career in local government. However, there is no evidence that these strategies have been implemented or evaluated for their effectiveness. While there have been no formal evaluations of the plan itself, council advised it has been effective in informing decisions about staffing levels when preparing the annual budget, identifying gaps, career planning for existing staff, and potential replacement of key staff—due to pending retirement, for example.

Strathbogie completed an organisational review in January 2011, which included voluntary redundancies, the creation of several new positions and the development of a new organisation structure. The review recommended that Strathbogie develop a workforce plan, initially for outdoor staff, and then the whole organisation. However, council has not yet done so.

Councils also outsource positions, including statutory roles, such as building surveyors and planning officers. Councils advised that these positions can be difficult to fill and that this may be due to the remuneration offered being uncompetitive in the current employment market, applicants not wanting to relocate to regional areas, or only requiring part-time positions for these professions. While Yarriambiack advised that staff recruitment was not an issue, they also outsource these statutory positions. Outsourcing may address the issue in the short term, and maintain ongoing service delivery, however, councils have not assessed whether this is more cost effective than employing staff directly. It is also not addressing the core problem of recruiting and retaining staff and may not be sustainable in the long term.

3.3.5 Population ageing and/or population changes

Population ageing and/or population changes—such as high growth or decline—can present challenges to small councils. Population changes can impact on councils' rating base and change service delivery needs. Population decline can also result in higher unit costs of service delivery because of the fixed nature of some costs. Rapid population growth can place significant financial pressure on councils to put new or expanded services in place. Given declining and ageing populations, continuing to increase rates and charges may not be sustainable for some councils.

Figure 3C summarises the trends and forecasts in population changes for the audited councils from 2001 to 2031. It shows that with the exception of Towong, there are consistent trends for these councils across the 30-year period of either increasing (Golden Plains and Strathbogie) or decreasing (Buloke and Yarriambiack) populations.

Figure 3C

Past, current and projected populations, 2001 to 2031

|

Council |

Population in 2001 |

Population in 2011 |

Percentage change 2001–11 |

Projected population in 2031 |

Percentage change 2011–31 |

|---|---|---|---|---|---|

|

Buloke |

7 331 |

6 925 |

–5.5 |

6 519 |

–5.8 |

|

Golden Plains |

15 101 |

19 014 |

+25.9 |

26 870 |

+4.1 |

|

Strathbogie |

9 648 |

10 060 |

+4.3 |

11 085 |

+10.2 |

|

Towong |

6 331 |

6 276 |

–0.9 |

6 552 |

+4.4 |

|

Yarriambiack |

8 311 |

7 498 |

–9.8 |

6 900 |

–8.0 |

Source: Victorian Auditor-General's Office.

Buloke and Yarriambiack have ageing populations, which together with population decline, raises particular sustainability issues for these councils. Growth rates in Golden Plains will result in it no longer being classified as a small council in the future.

Strategies

Buloke has developed a draft Positive Ageing Strategy 2013–19 to guide it in responding to the projected rapid growth of its aged population, but it does not address continuing population decline. While Yarriambiack had a 2009–12 Economic Development Strategic Plan that aimed to promote economic development in the shire, this plan contains limited analysis on population decline and does not directly link actions to address this issue.

Golden Plains has implemented strategies to deal with both a growing and ageing population. The council's 2012–16 Ageing Well in Golden Plains Strategy and Action Plan provides a detailed analysis of the shire's population demographics. The main aims of the plan are to enable the council to effectively respond to population growth, and to inform the direction, development and delivery of its aged services and programs. To assist in meeting growth in the number of young families, Golden Plains has implemented service improvement plans for kindergarten clusters and maternal and child health services.

Strathbogie is currently developing an Economic Development Master Plan 2013–17 to guide the future of economic development in the shire. The plan is expected to include strategies to promote consistent population growth.